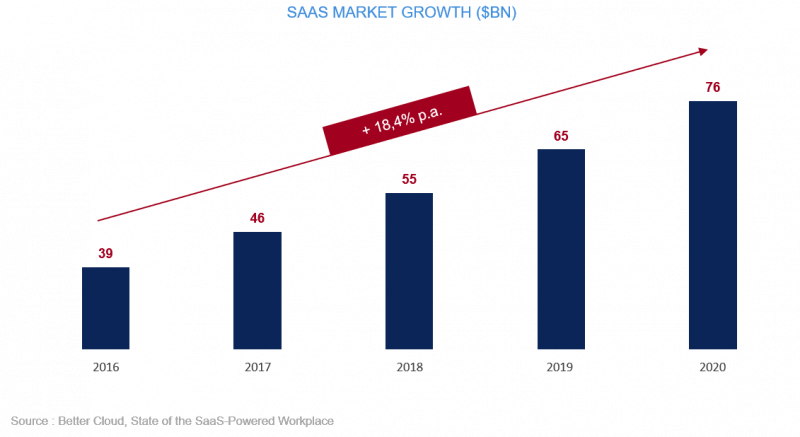

The market for SaaS (Software-as-a-Service) is expanding at 18,4% p.a. (2016-2020), and is forecast to be worth c. $76 billion worldwide by 2020. There are a large number of small players in this dynamic market, which will continue to fuel market consolidation and M&A activity moving forward. We are seeing both strategic and financial investors aggressively target the sector, which is supporting high (double-digit-plus) EBITDA multiples in the mid-market across Western Europe.

Transactions in the SaaS industry are growing in volume by c. 25% YoY, with around half of M&A deals including Private Equity. The strong appetite from both strategics and PEs for SaaS businesses is being driven by solid market fundamentals and the industry’s attractive business model case, which includes:

- Sustainable fast growth

- Recurring revenues

- High margin potential

- Maturity of the business model: 20-year track record

What is SaaS?

Software-as-a-Service is a software distribution model in which a third-party provider hosts applications and makes them available to customers over the Internet – it is one of three main categories of cloud computing, alongside Infrastructure as a Service (IaaS) and Platform as a Service (PaaS).

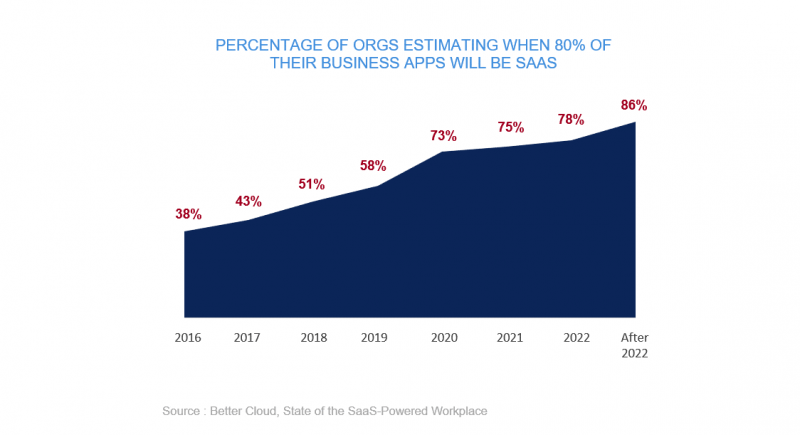

By 2022, 78% of all companies will be running their business applications as SaaS

Why SaaS?

Major benefits from SaaS solutions include:

- Limited upfront cost compared to legacy systems

- Reduces operational costs

- Scalable and flexible: easy to add and remove users or functionalities

- Remains modern and relevant: easier and faster upgrades

- Improves working processes

- Allows for collaboration in large or decentralized teams

- Easy-to-use: saves time for setup and training

- Provides easy access to valuable data

- Mobile-optimized

- Connects easily with third-party apps, and allows customized connections

How to value a SaaS business?

The keen investor interest in the sector is translating into high valuation multiples, typically above 4x revenues and 15x times EBITDA on average. This average hides some strong differences between the lowest and the highest valuation multiples, from less than 5x EBITDA for the smallest niche businesses with stable one-man-led operations, up to more than 10x revenues for unicorns. In this context, an entrepreneur or shareholder of a SaaS business may wonder which basis of valuation would be the most relevant for their business?

In most cases, EBITDA seems to be the best proxy for the business’ future cash flow, and thus, for the valuation.

But when the business is growing larger, with a high revenue growth rate (> 50% YoY), EBITDA might be too low (even close to 0 or less), as it is impacted by strong upfront investments which are all expensed in current EBITDA. Owing to the recurring revenue model, the profits will expand significantly as soon as the business matures and starts to spend less on its fast growth. Some strategic acquirers might also consider changing the cost structure of the business while integrating it into their group post-acquisition, which will also heavily influence the EBITDA and the future earnings of the business. In some such cases, it therefore makes sense to use revenues to reflect the value of an SaaS business, more than EBITDA.

Then the sustainability, scalability and transferability of the business will, amongst other criteria, strongly influence the multiple. More precisely, the multiple will depend on:

- The market segment growth potential and the potential growth of the company’s market share,

- the recurring revenues (measured through the annual recurring revenue (ARR), or through the monthly recurring revenue (MRR)),

- the churn rate and the customers’ loyalty/dependence on the solution,

- the total potential value that each customer should create over the whole period of service, measured through the ‘Lifetime Value’ (LTV) and ‘Customer Acquisition Cost’ (CAC)

- the maturity of the business model

- the barrier-to-entry vs the competition

- the age of the technology and the potential technological debt

- etc.